Your First Paycheck Quietly Sets Financial Defaults

I’m starting 2026 by focusing on foundations. Not resolutions, not optimizations, but the systems that quietly shape outcomes over time. Very few people rely on memory to show up to important meetings. Instead, they rely on a calendar. Once something is scheduled, the decision is made. You are far more likely to show up because the system is doing the work for you. That is the role a system plays. It quietly removes decisions before they become a problem.

Money works the same way. Financial outcomes are rarely driven by discipline alone. They are driven by systems and defaults that operate quietly in the background. That is why nearly 4 in 10 Americans with access to a 401(k) do not contribute to it at all. Not because they do not all want to save, but because no system was set up to make saving automatic.

⚙️Why a Financial System Matters

Many people dream of winning the lottery. The appeal of a sudden, life-changing amount of cash is obvious. Yet there are countless stories of lottery winners going broke within a few years due to a lack of structure & system.

In a quieter but very real way, a similar dynamic plays out after graduation. Many post-MBA and post-graduate roles come with a dramatic increase in income, often two to three times pre-MBA salaries. This increase is well-deserved, but it also introduces more financial decisions, more accounts, and more complexity. At the same time, graduates are navigating significant changes beyond money with new cities, careers, and social circles, all while returning to a demanding work schedule with far less free time to devote to managing finances.

In that environment, financial decisions get made quickly and often with an “I’ll fix it later” mindset. However, this is when financial defaults such as contribution rates, spending habits, and account structures are set. Not because you planned them, but because you were busy. Without a system in place before your first paycheck arrives, higher income doesn’t simplify your finances, it amplifies the chaos. The easiest time to build a financial system is before your first paycheck hits.

💼What Changes When Your Job Starts

The obvious thing happens first. You start making money (finally yay). That part is great, and it is well deserved. But alongside that income comes something less visible: a rapid shift in spending patterns and the establishment of new lifestyle expectations. Experiences that were previously out of reach become affordable. Travel gets upgraded (First class baby). Fine dining becomes more frequent (Did someone say Delbar on a Tuesday) None of this is inherently bad, but these early choices quietly establish a new baseline for how money gets spent that is incredibly sticky.

At the same time, the administrative side of your finances expands quickly. You receive emails about opening a 401(k). Family and friends suggest opening an IRA. You might open a brokerage account, an HSA, or sign up for insurance accounts you didn’t even know existed. All of a sudden you have a ton of new accounts to keep up with in addition to your existing accounts. Each of these accounts comes with additional decisions, often made quickly. Contribution rates are a good example. You may have heard that saving 10 to 15% in your 401(k) is reasonable, or your employer may automatically enroll you at a specific rate (say 5%).

One of my favorite researchers in this area of work is a Yale professor, Dr. James Choi. His research shows that a company’s default contribution rates and structure strongly anchor long-term behavior. In one study, his research shows that automatic enrollment increased employee participation to 85% from 35% for those that had to manually enroll.1 The takeaway is not that people do not want to save. It is that when saving & investing is not automated early, it often does not happen at all and “later” rarely turns into action.

Undoing a system is far more difficult than setting it up correctly from the start. You do not need to predict the future to build a Simple Financial System. Its job is to remove as many decisions from your everyday life as possible. Right now, before starting your new job, is the easiest time to formulate a strategy.

🧠The Design Principles of a Simple Financial System

A Simple Financial System is a small set of accounts, rules, and automations designed to work for you, not against you. It can be summarized by three principles: purpose, automation, and low maintenance. Purpose defines what each account is for. Automation makes the right behavior happen by default. Low maintenance ensures the system continues to work even when life gets busy.

Principle 1: Purpose

Every financial account should exist for a specific reason

Each account should have one job and one time horizon. Problems arise when a single account is used for multiple things. For example, using an emergency fund to pay for a large vacation makes it difficult to track progress toward saving for actual emergencies. Similarly, using the same account to hold emergency savings, receive paychecks, and pay bills is not inherently wrong, but it adds unnecessary reconciliation.

When each account has a clear purpose & job, decisions become easier and mistakes are harder to make. This applies beyond checking and savings accounts to investment accounts as well. Each investment account should also have one job, such as funding retirement or a future down payment on a house, and a clear time horizon, whether that is immediate spending, five years from now, or decades in the future.

Principle 2: Automation

You should not rely on willpower to do the right thing every month

A system works best when the right behavior happens automatically and the wrong behavior requires effort. Instead of trying to remember to invest whatever is left at the end of the month, set up automated contributions that occur before money ever feels available. When savings and investing happen first, you can confidently spend what remains in your account and take that decision away from your mental load.

In practice, this means 401(k) contributions are taken directly from your paycheck and IRA contributions are set on autopilot. Automation does not eliminate all decisions, but it removes friction. Over time, automation consistently beats motivation.

Principle 3: Low Maintenance

Your system should still work even if you ignore it

A well-designed system should continue to function if you get busy at work, go on vacation, or experience an unexpected life event. It should not require constant monitoring, frequent manual transfers, or regular adjustments to stay on track.

Low maintenance also matters when money involves more than one person. If you are married (like me) or share finances with a partner, a simple system creates consistency if anything were to happen to the partner that manages finances and also lowers the entry barrier for the partner who may be less interested in day-to-day financial decisions but still wants to be involved in conversations. At its best, a low-maintenance system makes money easier to manage, not another thing to worry about.

That is it. Three principles. The goal of a Simple Financial System is not to get every decision perfectly right, but rather to reduce the chance of mistakes, limit regret, and create a structure that allows you to focus on life by making fewer financial decisions.

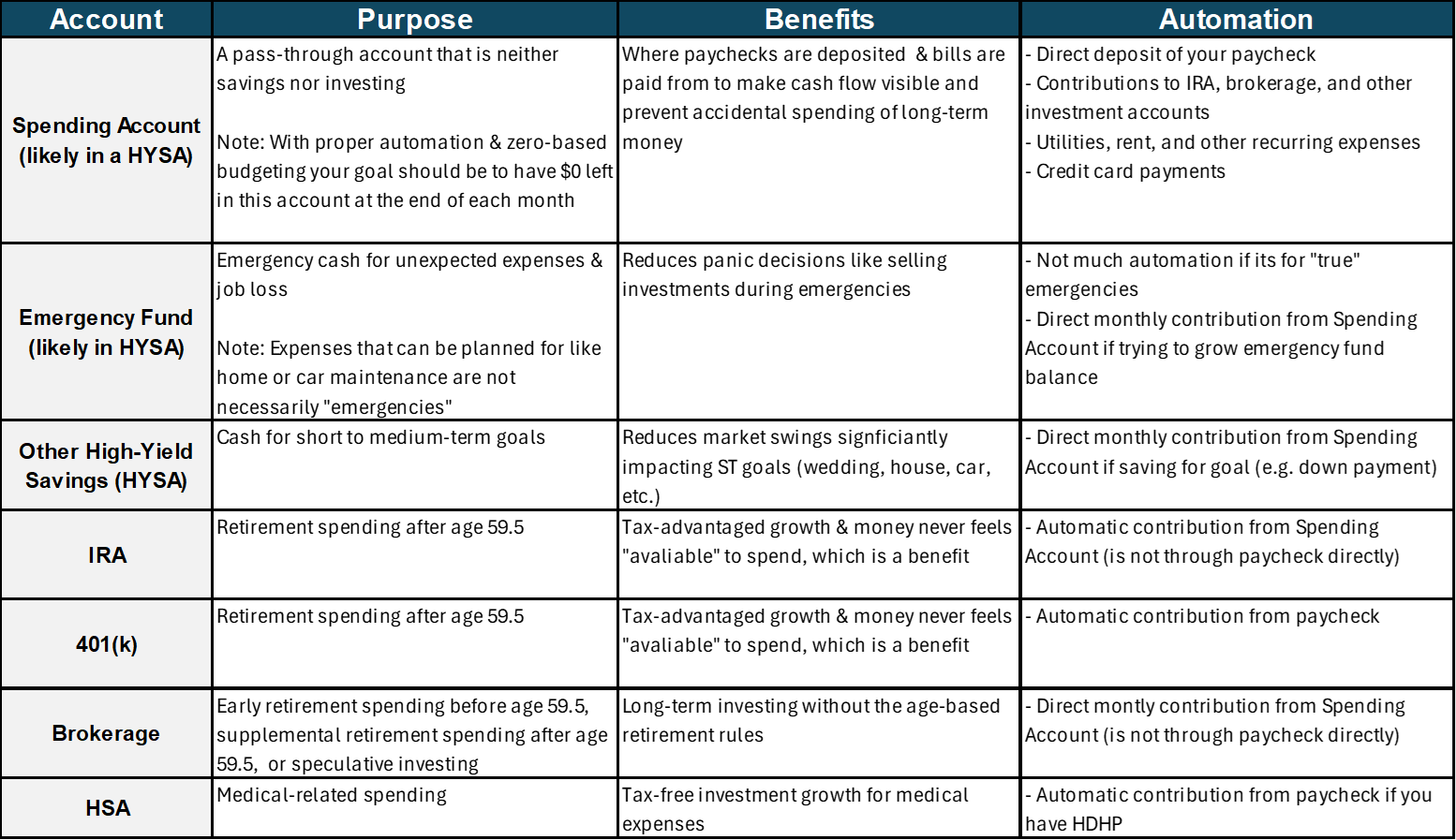

🏦The Core Accounts that Matter Most to a Simple Financial System

I will not be covering which bank, firm, or investment funds are best to use in this blog. Instead, this section focuses on which accounts matter most for a Simple Financial System and the role each one plays for most graduates.

The key idea is that financial accounts exist to separate time horizons and behavior. When different goals share the same account, decisions become harder and mistakes more likely. When each account has a clear role, the system becomes easier to understand and easier to maintain.

Below is a table outlining the core accounts that most MBA graduates should have or consider opening, along with the purpose, benefits, and potential automation flows for each:

Each of these accounts serves a distinct function within the system. Together, they create clear boundaries, support automation, and allow money to flow with minimal ongoing effort.

🛠️How to Implement a Simple Financial System

Now that we’ve covered why a Simple Financial System matters, how it is designed, and which accounts form the foundation, the next question is straightforward - how do you actually put this into practice? Below is a structured process to do exactly that.

Step 1: Personal Finance Review

Understand what you have already

Start by taking inventory of all your existing financial accounts. This includes checking and savings accounts, investment accounts, 401(k)s, IRAs, HSAs, and any other accounts where money lives. Write down the purpose of each one.

Do the same for your credit cards. Review their benefits, fees, and why you originally opened them. This exercise is the financial equivalent of reviewing your subscriptions. The goal is simply awareness, not immediate action.

Step 2: Consolidate, Remove Friction, and Fill Gaps

Lay the foundation for simplicity

Next, review the list of accounts you compiled above and ask two questions of each one:

Is this account still serving the purpose it was intended for?

Would I open this account today if I did not already have it?

If the answer to either question is no, consolidation or removal is worth considering. Review accounts that share duplicative purposes. Multiple accounts serving the same purpose often add complexity without adding value. For example, old employer 401(k)s may be candidates for consolidation into an IRA or your new employer’s plan.2 Bank accounts at your hometown bank that you no longer use or credit cards with annual fees and no clear benefit may also be worth closing or downgrading.

At the same time, you may notice gaps. Perhaps you plan to buy a home in a few years and want a dedicated account to save. In that case, opening a separate high-yield savings or investment account with that specific purpose can add clarity rather than complexity.

Accounts are the foundation of a Simple Financial System. This step may take some effort upfront, but it pays dividends in reduced friction, mistakes, and heartburn in the future.

Step 3: Automate, Automate, Automate

Automate everything up until spending

With the foundation in place, the final step is to automate how money flows through the system. Start by identifying how each account will be funded. Some contributions, such as your 401(k), will typically be funded directly through payroll. Others, such as an IRA, brokerage account, or savings goal, may be funded from your Spending Account. Once you decide the flow, set these contributions up as recurring, automatic transfers on their respective platforms.

When investing and saving happen automatically, the money never feels available to spend in the first place. This naturally leads to less wasteful spending and constant decision-making or mental tradeoffs. That is why the guiding rule here is simple: automate everything up until spending.

⏭️I’ve Set up a Simple Financial System. What’s Next?

A quick summary of what a Simple Financial System now handles. Retirement contributions happen automatically without effort. Investing happens without constant decisions. Emergency savings are protected. The biggest mistakes are far less likely to occur. That is the point of the system. Once your paycheck hits, the process is largely automatic. Contributions to your 401(k), IRA, brokerage, savings goals, and loan payments are already accounted for. What remains is the part of money that requires choice: spending.

At this stage, your Spending Account becomes the focus. Rent, groceries, travel, dining, and everything else flows from here. How you organize and track this spending is a personal decision. This is also where budgeting enters the picture. Not as a set of rigid rules, but as a way to understand how you actually use money. A clear view of your spending will inform the remaining investment decisions the system does not solve on its own, especially contribution rates (i.e. how much money you can “afford” to invest).

It is easy to set up a 401(k), however, it is much harder to know how much you should contribute without understanding your cash flow first. That’s why I say “automate up until spending”. But don’t worry, you can automate “spending” too, but not until you set your spending budget.

In the next post, we will walk through how to think about budgeting in a way that reflects real behavior, how spending data can inform contribution decisions, and eventually we’ll cover how savings rates are the most powerful driver of financial independence.

🧭Summary: Building Control Through Structure

A Simple Financial System is not about optimization or perfection. It is about structure & limiting mistakes. By clearly defining the purpose of each account, automating the most important decisions before money ever feels available, and keeping the system low maintenance, you remove much of the friction that causes financial stress & regrets. The goal is not to predict every future expense or get every choice right, but to build a system that works quietly in the background and allows you to focus on life instead of managing money.

P.S. I’ve linked a blog post from Money with Katie that covers a similar topic (money mapping) for any visual learners.

⚠️A Practical Note on Automation & Cash Flow

Automation is one of the most powerful parts of a Simple Financial System, but it does introduce a few cash flow considerations worth being aware of:

Automated payments can fail if cash flow timing is misaligned. For example, if rent, student loans, or credit card payments are scheduled to withdraw before your paycheck is deposited, your account may not have sufficient funds at the time the transaction processes. Two simple ways to manage this:

Keep a small buffer in your Spending Account instead of treating it as a zero-balance pass-through

Schedule automated transfers and bill payments to occur after your paycheck hits (if possible)

The goal is not optimization, but reliability.

Automatic enrollment refers to when employees are enrolled in a 401(k) by default, with no action required on their part

There may be tax implications associated with moving certain accounts. Consult with your CPA prior to taking any action.